As income tax rates have risen, so has the value of the tax exemption that accompanies municipal bonds. As a result, more investors are looking to take advantage. At the same time, the municipal bond landscape has changed significantly in the past several years, making the case for an active, research-driven approach to investing.

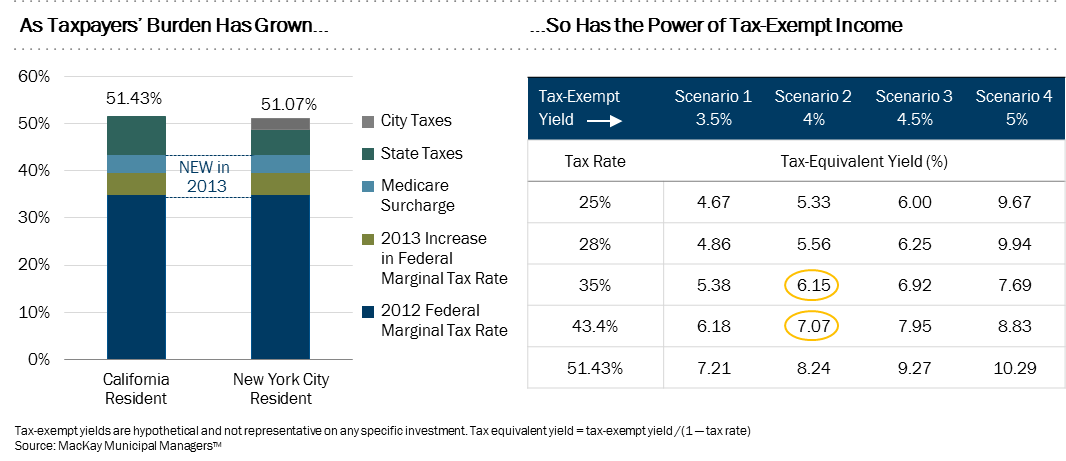

After many years of unchanged tax rates, many U.S. taxpayers have felt the dramatic impact of higher taxes in the last two years. For earners in the top income bracket, the 2013 adjustment in federal tax raised the marginal rate to 39.6% from 35%. The Medicare surcharge (which doesn't apply to municipal bond investment income) added another 3.8%, for an overall total of 43.4%. Proportionally, that's an increase of almost 24% in marginal tax rates for high earners. Add to this state and city taxes, and some taxpayers are facing a marginal rate of more than 50 cents in the dollar.

See: 15 Worst States for Income Taxes

Advertisement

In other words, the value of tax free income just went up. Last tax year, a lot of people didn't realize the implications. But this year it's beginning to sink in more and more. When you start looking at the tax equivalent yields that the muni market offers—especially in states like New York or California—a yield of 4% exceeds 8% on a tax-equivalent basis. And that's in a relatively safe, secure asset class.

For an apples-to-apples comparison between muni bond and taxable bond yields, the thing to look at is the tax-equivalent yield. Take the example of an investor in the 43.4% tax bracket who wants to take home a yield of 4%. To do this in the muni market, he or she would need a portfolio of bonds yielding 4%. In the taxable bond market, he or she would have to earn a tax-equivalent yield of 7.07% to clear 4% in tax-free income. In 2012, with a maximum marginal rate of 35%, the tax equivalent yield would have been 92 basis points less, at 6.15%.

INVESTMENT GRADE

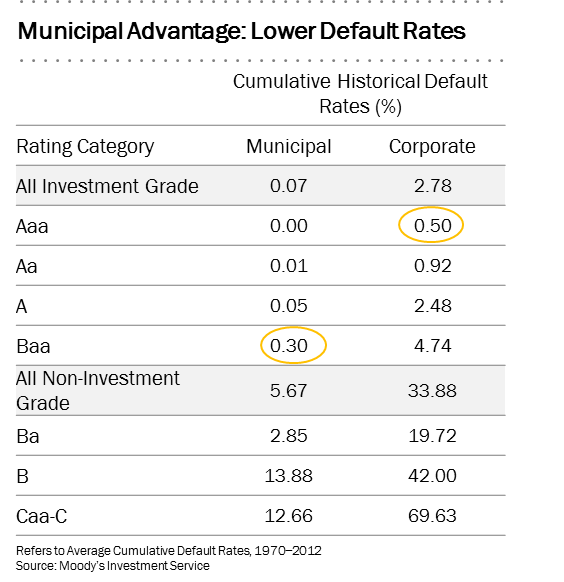

In today's markets, a yield of 4% may likely be achieved by investing in an actively managed portfolio with credit quality primarily in the investment-grade range. But to get to 7.07% in the taxable market, one would require a much more aggressive risk profile, in other words reaching down the credit spectrum into lower-rated corporate bonds. For example, the Barclays US Corporate High Yield index currently yields about 5.9%, but with an average credit quality of B1/B2. It's also worth noting that, for any given credit rating, muni bonds have historically experienced lower default rates than corporates. In fact, on Moody's rating scale, since 1970 Baa-rated munis have had lower cumulative default rates than Aaa corporates.

CHANGING LANDSCAPE

In years past, the case could be made for passive, buy and hold portfolio strategies in which investors built a “ladder” of various maturities and pretty much forgot about them. Today, investors face new challenges. The municipal bond landscape has changed dramatically in recent years, with limited liquidity, reduced dealer inventories, higher transaction costs and a greater need for full-time credit research. Investors are also realizing that municipal bonds can be employed in a number of ways — for income strategies, for capital preservation and for more return-driven strategies. An active approach can go further to unlock those possibilities, to manage new risks and exploit new opportunities.

Bond investors have had the benefit of a 30-year downward trend in yields. Now, amid expectations of rising rates, they have to think about managing interest-rate exposure, and about how much they have in different maturity buckets. Investors need the flexibility to move up and down the yield curve, depending on which maturities offer the best relative value. For those holding individual municipal bond positions on a direct basis, it can be difficult to capitalize on the opportunities in the same way that an actively managed strategy with deep credit research can.

We expect a flattening of the yield curve to cause dislocations and spread widening among high-grade bonds on the short to intermediate part of the yield curve and, as a result, we believe this segment of the market should be avoided in 2015. Because they are more highly correlated to Treasury securities, AA and AAA-rated municipal bonds in the 3- to 7-year maturity range have a higher exposure to potential interest rate hikes by the Federal Reserve than most other segments of the municipal market. Getting defensive on rates without sacrificing income by focusing on cushion (high coupon/premium bonds) is our preferred portfolio structure. This will cause actively managed portfolios to outperform passive municipal bond ladders in terms of total return and current income.

HIGHLY INEFFICIENT

The municipal bond market is a highly inefficient one, in which an active portfolio management approach is both a necessity and an opportunity. With over a million individual issues, no exchange-traded market but many broker-dealers, and a preponderance of individual investors rather than institutional buyers, the muni market is prone to information gaps and mispricings. Compared with more efficient markets where most of the information is “priced in,” munis can offer a real competitive edge to full time municipal bond managers who do their research and nurture a wide network of industry contacts.

This has become even more relevant in recent years as volatility has flared up around Detroit, Stockton, Calif., and Puerto Rico. Volatility feels uncomfortable, but it also rewards investors who can identify the opportunities and move fast enough to exploit them. There will always be headline events like Puerto Rico, but chances are that investors' mindset will be different. Instead of asking whether their manager is avoiding the problem area, investors are instead starting to ask what their fund manager is doing to capitalize on it.

John Loffredo is is co-head of MacKay Municipal Managers and manager of the MainStay Tax Free Bond Fund.