Only 15% of employees using tax-deductible health savings accounts are maxing out their contributions, and there's still a good deal of uncertainty about how best to fund the accounts.

According to a recent analysis of HSA data by the Employee Benefit Research Institute, fully 15% of the HSA accounts in its database had received the maximum contribution in 2013. The data pool EBRI studied comprises 1.5 million HSA accounts and $2.7 billion in assets.

Health savings accounts are becoming a bigger part of workers' lives as employers shift health care costs to employees. These HSAs work alongside high-deductible health care plans, and employees are expected to cover qualified medical costs using the account.

Advertisement

On the surface, the 15% figure is a win. “I found that 15% to be encouraging,” said Kevin Boyles, vice president of business development at Ascensus, a retirement plan service provider. “The number of people hitting the maximum [contribution in 401(k) plans] is around 12%, and those accounts have been around for over 20 years.”

Nevertheless, the figure also suggests that there is a knowledge gap for employees and employers on the best ways to fund an HSA.

FUNDING HURDLES

First things first: The reality is that there is only so much paycheck to go around. Many rank-and-file employees already struggle to make double-digit contributions to their 401(k) plans, so hitting the max contribution of $18,000 is a lofty goal.

Workers are also contending with a competition for their dollars now that HSAs are in the picture. Contribution limits for these accounts are capped at $3,350 for individuals and $6,650 for families this year, which is lower than the cap for 401(k)s, but still an ambitious goal for many.

Though employer matching contributions to 401(k)s can encourage workers to kick more money into their retirement plans — promising a 50% match if someone contributes up to 6% of salary will encourage workers to stretch for that 6% — EBRI's data is showing that this isn't necessarily the case when it comes to HSAs.

In 2013, 14% of HSAs with an employer contribution reached the maximum contribution level, compared with 20% of the accounts that didn't have an employer contribution.

“This is a guess, but people who receive an employer contribution may not feel the need to contribute themselves, and that mentality may be playing into this,” said Paul Fronstin, director of the health research and education program at EBRI. “Or they may be reliant on the employer for the contribution.”

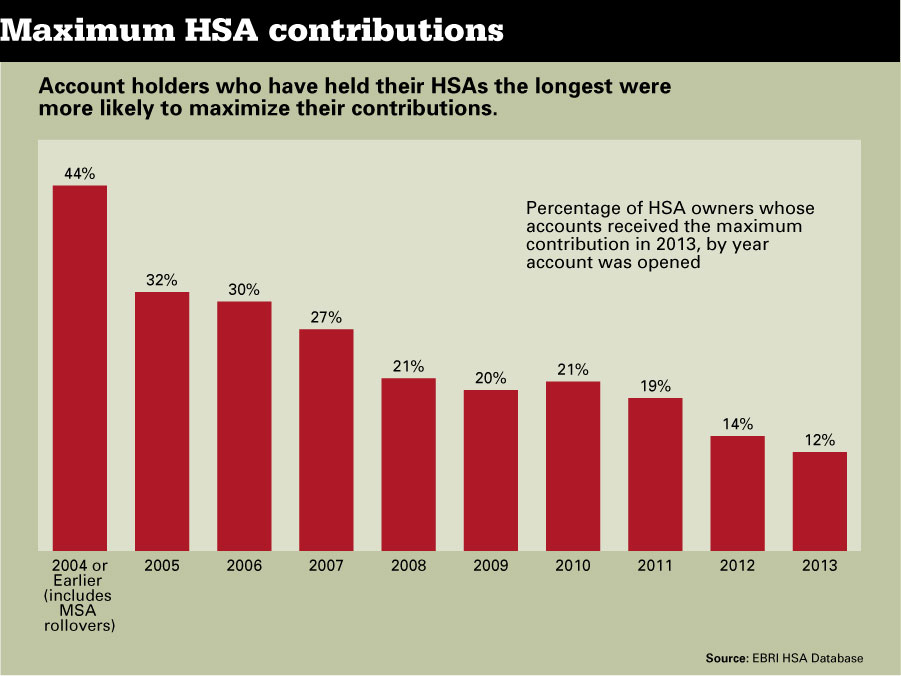

Another thing to consider is that account holders who've held an HSA for many years tend to contribute more to those accounts. Forty-four percent of HSA owners who have had their accounts since 2004 or earlier reached the maximum contribution level in 2013, according to EBRI.

Those who reached the max without an employer's contribution might be more engaged or better aware of the tax benefits that health savings accounts offer, said Mr. Fronstin.

STRATEGIES TO BOOST FUNDING

Aside from giving workers raises, employers could consider other strategies to nudge employees into raising their HSA contributions. Contributions are tax-deductible if an individual — and not the employer — adds the money into the account. Meanwhile, contributions by the employer, plus those made through a cafeteria plan, aren't counted toward gross income.

“There may be opportunities to educate the employees about the value of contributing to the account that would increase contribution levels sooner,” said Mr. Fronstin. “You have all these rules that people aren't necessarily aware of simply because employers and HSA providers aren't spending a lot of time talking about them.”

Another point that ought to be discussed at the workplace is the fact that HSAs can work as a longer-term vehicle for medical expenses in retirement. “You can use it to fund premiums for long-term care insurance with a tax-free distribution,” said Mr. Boyles, noting that the HSA is the fourth leg of the retirement three-legged stool. The first three are Social Security, pension plans and employee savings.

The accounts will mean something different for each worker, based on demographics, income and current health status.

“The 62-year-old will think of it differently than the 28-year-old,” Mr. Boyles said. “It's key to understand that some people will use these accounts as an HSA [longer term] and others will use them as a glorified flexible-spending account with no use-it-or-lose-it provisions.”